Consideration of Taxes in the UK

In the United Kingdom, a person’s tax liability depends on where their assets and sources of income are located, as well as where they live and where their home is. It is a complicated and sometimes hard subject.

I would like to explain to you the rules in the consideration of taxes when coming to the United Kingdom in simple language. It will help you figure out which tax areas are affected when someone enters or leaves the United Kingdom. Then it gives a clear list of questions to ask to figure out how much tax a person has to pay in the UK. It ends with a short talk about international agreements and double tax relief.

Some Fundamental Guidelines

When it comes to taxes, a person who lives and has a home in the UK has the following tax status:

- Income tax (IT) on all earnings, no matter where they come from.

- Tax on capital gains (CGT) on all assets around the world.

- IHT (Inheritance Tax) on assets around the world.

In the same way, a person who has no ties to the UK and is neither a resident nor a citizen has the following tax status:

- Only pay income tax on income from the UK.

- No Capital Gains Tax (Conditions apply but check Part 4 for exceptions).

- Inheritance tax only applies to assets based in the UK.

Carefully review the aforementioned issues, do some brainstorming, and acknowledge that they will all lead to the following:

- Everyone who receives money from the United Kingdom must pay taxes on it, regardless of their status.

- People who reside outside the United Kingdom are exempt from paying UK CGT on (most) UK assets (but see Part 4 for exceptions).

- UK assets are always liable to UK IHT, regardless of the individual’s status.

UK source income consists of funds derived from UK assets, work performed in the UK, and trades conducted in the UK.

Land, buildings, and personal property are all considered assets in the UK. Assets in the United Kingdom include, among other things, funds held in financial institutions in the United Kingdom and securities registered in the United Kingdom.

Putting the Composition Together

The preceding rules raise three crucial questions:

- When does the United Kingdom tax income from outside the United Kingdom?

- When must gains on British and overseas assets be paid to UK CGT?

- How do non-British assets become liable to UK IHT?

This article explains in what order you should consider the most significant residency and domicile variables when answering these questions. Here are some brief descriptions of the rules used to determine a person’s residency and domicile.

Residence

The rules about residency are very specific and depend on how long a person has lived in the UK and what their situation is.

Figure 1 – Residence status determination

The Split-year Strategy

A person can either be a tax resident or a tax-non-resident in a tax year from 6-April to 5-April. In certain instances, however, the tax years of arrival and departure may be divided. Under split-year accounting, the year is divided between the United Kingdom and other countries. The individual is taxed as follows:

1. A UK resident on the portion of the income generated in the UK,

2. A non-UK resident on the foreign portion.

This impacts both the income tax and the CGT.

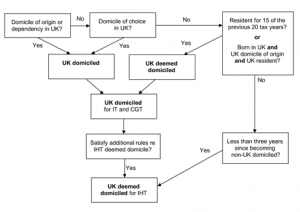

Domicile

In terms of income tax, CGT, and IHT, a person’s residence is crucial. People who do not reside in the United Kingdom may be considered residents for tax reasons.

Visiting England

A non-resident will become a resident if all ties to their previous nation are severed and they intend to remain in the UK permanently after moving there.

Leaving England

A person who has left the United Kingdom will lose UK domicile if:

1. all ties to the United Kingdom have been broken;

2. the individual intends to live in the new country permanently.

Deemed Domicile

Two types of presumed domicile exist:

1. One applies to income tax and CGT, while the other

2. is applicable to IHT.

Figure 2 – Status of domicile determination

(Guidance: ACCA Technical)

(The above blog is not advice so please get proper professional advice if you are in a similar situation).